Want to save

(or save more) for education?

Open a new KY Saves 529 account and we'll contribute to it too!

How much do we believe in your child's potential? Enough to help you invest in it. Until May 31st, we're adding $25 to every new KY Saves 529 account opened for children age 5 or younger with a minimum $25 initial contribution.1

So, if you've been thinking of saving (or saving more) for a college, trade, or vocational education, opening a KY Saves 529 right now is kind of a no-brainer. Here's all you do:

Don't have a KY Saves 529 account now?

- Open an account for a child aged 0-5 between May 1-31, 2024.

- Contribute an initial $25 minimum amount.

- When you do, we will contribute $25 into your new KY Saves account.1

Have a KY Saves 529 account already, but you want to open one for a new family member?

- Open another account for a child aged 0-5 between May 1-31, 2024.

- Contribute an initial $25 minimum amount.

- When you do, we'll add $25 to that new account.1

Use it for more than college tuition

- Eligible college, graduate school, trade and vocational school, and apprenticeship programs

- K-12 tuition2

- Loan repayments3

- Room and board

- Fees

- Computers and laptops

- Books

- Even things like tools, if required by the program

For rules and eligibility, please read the Official Promotion Rules.

1Funding is limited to the first 300 accounts opened for a beneficiary aged 0-5 years old between 5/1/2024 and 5/31/2024. Your initial contribution ($25 minimum) must be received by 6/30/2024.

2Expenses for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school, not to exceed $10,000 per student per year in the aggregate across all 529 Plans for such student. Since different states have different tax provisions, if you or your beneficiary, as applicable, are not a Kentucky taxpayer, the state(s) where you pay income tax may differ in its state income tax treatment of K-12 tuition expenses. You should consult your own state’s tax laws or your tax advisor for more information on your state’s taxation of withdrawals for K-12 tuition expenses.

3Principal or interest on any qualified education loan (as defined in section 221(d) of the Internal Revenue Code) of the designated beneficiary or a sibling of the designated beneficiary, up to a lifetime limit of $10,000 per individual. Note, if you make an education loan repayment from your Account, Section 221(e) (1) of the Internal Revenue Code provides that you may not also take a federal income tax deduction for any interest included in that education loan repayment.

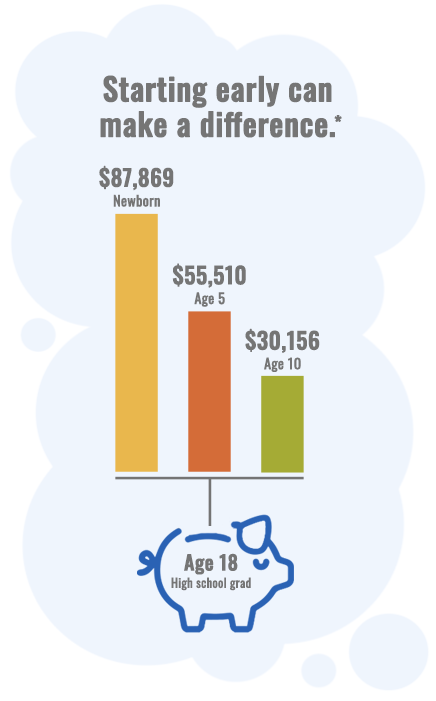

*Assumptions: $500 initial investment with subsequent monthly investments of $250 for a period of 18 years; annual rate of return on investment of 5% and no funds withdrawn during the time period specified. This hypothetical is for illustrative purposes only. It does not reflect an actual investment in any particular 529 plan or any taxes payable upon distribution